Portfolio Management Report February 2025: There are decades in which nothing happens; and weeks in which decades happen.

Europe preferred — capital flows are shifting

February 2025 was characterized by increased market volatility. While European equities continued to outperform US stocks, market uncertainty increased towards the end of the month. Geopolitical developments and an increasingly erratic US economic policy determined market developments. The initial relief following the federal elections in Germany gave way to a pragmatic assessment: The new grand coalition may appear more politically stable, but whether it will be able to overcome the structural economic challenges (especially in the shortest possible time) remains to be seen. A notable trend is the inflow of capital from the USA into European equities.

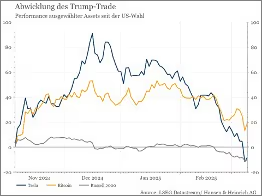

American investors are increasingly shifting, as valuations in Europe appear to be more attractive and economic prospects are stabilizing. As a result, European indices ended the month with positive signs, while the US markets recorded losses. The Nasdaq in particular had its weakest month since April 2024. The oft-quoted “Trump trade” — i.e. potential winners of Donald Trump's second term of office, such as small caps or crypto tokens — has largely unloaded (Figure 1). Whether this trend will develop into a sustainable reorganization of capital flows remains an open question. The latest Munich Security Conference made it clear once again that Europe is playing a reactive rather than formative role in the geopolitical upheavals of the coming years. The question remains whether Europe can strengthen its economic independence — the markets will react sensitively to this.

US tariffs escalate: Trump takes two steps forward, one step back

Figure 1: Performance of Tesla, Bitcoin and Russel 2000 since the US election. The oft-quoted “Trump trade” has largely unloaded.

The US government's trade policy continues to create increased uncertainty. For a long time, the market had assumed that Trump would primarily use tariffs as a bargaining chip. But with the implementation of the 25% punitive tariffs on steel and aluminum imports from Canada and Mexico (and also tariffs against China), there is growing concern that protectionist measures could solidify. In particular, the fluctuating communication and announcement strategy of the US administration is weighing on the market environment. Tariffs are temporarily enacted, then postponed again — this uncertainty makes it difficult for companies and investors to plan. In particular, punitive tariffs against direct trading partners Mexico and Canada could drive inflation in the USA in the medium term. It was precisely the rising cost of living that had contributed significantly to Joe Biden's election defeat during the election campaign — and they could now also torpedo Trump's economic policy plans. The corporate world is increasingly skeptical. The head of the American car company Ford Jim Farley commented on Trump's previous economic policy as follows: “We see a lot of costs and a lot of chaos.” The expectation that Trump will also impose punitive tariffs on EU imports on March 12 is particularly alarming for European investors. The European Union has already prepared product lists for countertariffs. At the same time, you have to be aware that we will not find a blueprint in Trump 1.0 to assess Trump 2.0. Donald Trump will also have to accept that the framework conditions have changed massively compared to back then. In contrast to the first presidency, US stocks are now historically overvalued, interest rates are twice as high and the budget deficit is historically high despite a good economy. Capital markets are quite pragmatic in this regard and this explains, after the initial euphoria, the declines in share prices at the end of the month.

Interest rates: ECB focuses on interest rate cuts, Fed remains cautious

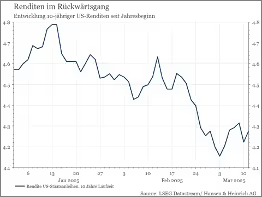

Interest rate policy remains a decisive factor for market movements. The divergence between monetary policy in the USA and Europe continues to grow. The ECB cut its key interest rate by 25 basis points at the end of January and will continue this rate in March. The main reason is the weak economy in the Eurozone, particularly in Germany. Inflation has stabilized between 2.3% and 2.5% (and is therefore above its own target), but is currently playing a minor role for the ECB. In the USA, on the other hand, the Federal Reserve remains cautious. While four interest rate cuts were expected for 2025 at the beginning of the year, the forecast has now fallen to a reduction in autumn. Yields on ten-year US government bonds fell from 4.6% p.a. (mid-February) to 4.2% p.a. (Figure 2) — a remarkable move for the bond market. The Fed will therefore soon have to decide whether this decline is a harbinger of an economic slowdown that requires a monetary policy response.

Technology sector: First signs of fatigue

Developments in the technology sector point to a possible sector rotation. While companies like Nvidia reported impressive quarterly figures, market reactions were disappointing. This suggests that some positive expectations have already been fully priced in. The euphoria surrounding artificial intelligence (AI) is also showing initial cracks: Microsoft and other well-known industry representatives report declining interest in AI applications. In addition, alternatives are now being followed, such as the Chinese DeepSeek, which promise a fraction of the costs. This will have an impact on the willingness to accept increased reviews.

Outlook: Volatile weeks ahead

The next few weeks will be important for capital markets. The focus is on the following topics:

- Will the mutual threats of punitive tariffs expand into a trade war or will agreements follow in which both sides can save face?

- As a result of falling inflation, will central banks be able to stimulate markets with the prospect of lower interest rates?

- Has there been progress on the Ukraine issue or will the conflict remain a burden factor for the economy and markets?

Strategic recommendations for investors

Figure 2: Development of 10-year US yields since the beginning of the year.

As long as key issues remain unresolved, we rely on a balanced strategy between defensive sectors (health care, utilities and consumer staples) and selectively high-margin growth stocks. The first category offers relative stability, the second can implement competitive advantages through high margins (as an effective moat). In addition, you should keep an eye on the global debt problem and prepare for significantly larger fluctuations in the bond markets. The debt ceiling will become an issue in the USA in mid-March and offers US Democrats the opportunity to publicly stand up to Trump. A new monetary policy strategy appears to be emerging in Europe: government investment as a stimulus. The capital market will monitor and evaluate this accordingly.

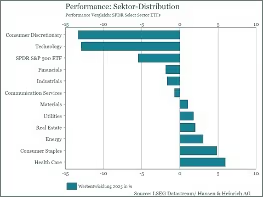

Figure 3: YTD performance comparison of “SPDR Select Sector ETFs”.

Conclusion: A balancing act between opportunities and risks

February 2025 was characterized by geopolitical tensions, interest rate expectations and a changing market structure. While European stocks maintain their relative strength, the situation on Wall Street remains tense due to debt, tariffs and inflation. We are continuing to be selective for our investors and are preparing for more volatile markets. Diversification into market leaders in promising industries continues to protect against emotional decisions and illusory activity.

The Hansen & Heinrich Universal Fund (current equity ratio 93%) was able to continue the positive market development at the start of the year and also closed with share price gains in February. While the general stock indices posted stable gains (Europe) and slight losses (USA), there were sometimes significant movements of more than 15% (in both directions) at individual stock level. We have selectively used these market distortions to make targeted adjustments to the portfolio. Examples include acquisitions in American-Irish Accenture and TSMC from Taiwan, which we saw attractive entry opportunities. At the same time, inventories in AbbVie, Booking and Siemens were successfully reduced in connection with the expiration date. Alibaba's stock has seen a remarkable recovery in recent months. After several years of regulatory headwinds, the recent rapprochement between founder Jack Ma and Chinese leaders points to a more stable business environment. President Xi Jinping reaffirmed the importance of private companies, which is seen as a positive signal for investors. Strategically, Alibaba is increasingly focusing on artificial intelligence and cloud computing. The company is pushing ahead with the development of its Qwen 2.5-Max language model, which, according to internal tests, surpasses leading US models such as GPT-4o. The cooperation with Apple also strengthens Alibaba's position as an innovative leader in the Chinese market. The restructuring into six independent business areas increases strategic flexibility and could unlock long-term value potential. Despite these positive developments, significant risks remain. Economic uncertainty in China, cautious investments by the private sector and the dominant role of state-owned companies could dampen growth momentum. In addition, geopolitical tensions remain a significant factor of uncertainty. For us, however, Alibaba remains an interesting investment, as the current market situation offers attractive volatility. In particular, this provides above-average standstill income, which allows us to tap into additional return potential in a targeted manner. We are keeping Alibaba in our portfolio as an opportunistic addition with selective risk management and continue to make targeted use of market movements for opportunistic adjustments.

The H&H Endowment Fund (current equity ratio 36%) continued its positive development in February. Through broad diversification through fixed-income bonds and shares from sustainable high-quality companies, the fund has proven to be a stable pillar for long-term investors. Despite current political and media headwinds in the USA, sustainability remains a key success factor for long-term investments. We are convinced that a good conscience and return are not mutually exclusive. While interest in ESG investments is declining in the USA, Europe remains a stable market for sustainable strategies. Endowment funds in particular are benefiting from this trend, as they combine financial returns with social benefits. Capital market data shows that ESG-compliant investments are in no way associated with yield disadvantages — quite the opposite. Strategies that rely on high sustainability standards have often performed better recently than conventional investments. This is particularly relevant for foundations, as they not only preserve assets but also provide positive social impulses. Regulatory adjustments in the EU, in particular new transparency requirements, are helping to avoid greenwashing and offer investors greater security. In the fixed-interest bond sector, we were able to successfully build up positions from new issues in high-quality issuers such as ACCOR, Air Products, American Medical, Barry Callebaut, IBM, Johnson & Johnson and Linde. These issuers are characterized by solid business models and high credit ratings. On the equity side, our position in Eli Lilly in particular grew pleasantly. The company is one of the leading players in the global pharmaceutical market and impresses with innovative therapies in the areas of diabetes, oncology and neuroscience. In particular, the development of GLP-1-based drugs for the treatment of diabetes and obesity is driving growth. Experts predict that the market for these drugs could grow to 100 billion USD by 2030 — a promising prospect for long-term investors. Eli Lilly recorded sales growth of 32% to 45 billion USD in 2024 and expects similar momentum in 2025. The company's strong global market presence and innovative strength secure a leading position in the sector, while investments in new areas of application — such as the treatment of cardiovascular diseases — open up further potential. With a market capitalization of over €800 billion and a strong focus on research, Eli Lilly remains an attractive investment for long-term investors. At the same time, we are making targeted use of the current market volatility to manage short-term options in order to collect additional bonuses. These option premiums form an important part of the regular distribution component that our investors have relied on for years. With a consistent focus on sustainability, diversification and active management, the H&H Endowment Fund remains a reliable solution for investors who want to combine long-term capital preservation with a sustainable return perspective.

In WowiAssets (current equity ratio: 14%), we were able to participate in a number of new issues from attractive issuers. The focus for reinvestments was primarily on maturities of 4-7 years. New additions to the portfolio included bonds from renowned issuers such as T-Mobile US, Linde Plc, Air Products, Leasys, Barry Callebaut and Johnson & Johnson. Bonds from Banco Santander, Nordea Bank and Koninklijke KPN matured during the month. Thanks to the focused new investment, primarily in the range of 4-7 years, the remaining term of the pension portfolio was 4.12 years at the end of the month. The return on the bond portfolio was 3.49%, with an average rating of BBB+, as of 28.02.2025. For better guidance, it should be added that the yield on a 4-year federal bond as at 28.02.2025 was around 2.01%. On the equity side, we were able to take advantage of our position in Siemens. The company has recently benefited greatly from fantasies about accelerating the expansion of data centers and a continuing need to digitize industry. The business model benefits from a change from traditional production to a software company (software as a service) and thus earns significantly higher margins than in the past, which was also reflected in the expansion of the valuation. Recently, the initiation of a potential ceasefire in Ukraine was able to further boost the share price. At current levels, Siemens seems to be pricing in a lot of positive things. The share's valuation is above its historical valuation of the last 10 years. In addition, the performance of Siemens shares is characterized by pronounced seasonality. Accordingly, the majority of the capital gains are typically achieved in the fourth quarter until the dividend is paid. The company was able to make a promising change in recent years, sufficiently consolidate the consortium and was rewarded for this by the capital market. — A good time to take the first profit. As a result of further maturities in the area of equity bonds and occasional profit-taking, we are looking at the upcoming movements in March with the necessary calmness and composure. A conservative structure, increased monthly coupon income and a series of short-term bonds give us the necessary flexibility to be able to react to opportunities on the interest rate and equity market.

Your Hansen & Heinrich portfolio management