Portfolio Management Report March 2025: Capital Markets in Transition: Two Worlds, Two Paths

Hansen & Heinrich AG Portfolio Management Report — March 2025

Spring 2025 marks the beginning of a new chapter on capital markets: On both sides of the Atlantic, the economy and politics are regrouping — but in completely different ways. The political decisions on both sides of the Atlantic caused unrest on the capital markets. While the USA under President Trump is striving for a comprehensive reorganization of its economy, characterized by re-industrialization and fiscal consolidation, Europe is focusing on fiscal expansion and political emancipation. In Germany, the reform of the Basic Law is softening the debt brake — a historic step that is likely to change Europe's financial policy landscape. At the same time, President Trump is unleashing a tectonic shift in the US economy with his trade policy offensive and ambitious budget plans. Two worlds, two strategies: While Europe is struggling for new independence, the United States is relying on national self-assertion and economic self-sufficiency. Investors are feeling the growing nervousness — the times of supposedly easy profits are giving way to an environment that requires discipline, vision and adaptability.

Realignment of the US Economy: Self-Assertion as a Strategy

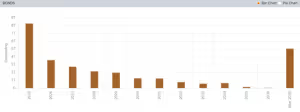

Based on the measures and political priorities introduced so far, three core objectives of economic policy orientation can be derived: fiscal consolidation, curbing uncontrolled migration and re-industrializing the country. Import duties play a central role in this. So far, the market has assumed that Trump's eratic tariff demands only serve as a negotiating tool. However, there is now growing evidence that these tariffs are being used as a significant source of revenue to finance tax cuts and as an incentive to relocate strategically important industries to the United States. In this context, it should be borne in mind that the administration must refinance around 40% of outstanding government bonds (approximately 12 trillion USD) within the next 18 months (Figure 1). With yields of just under 5% on ten-year US government bonds, there is a risk of noticeable burdens on the federal budget.

Figure 1: Maturity structure of US bonds. Around 40% of outstanding bonds will be refinanced in 2025 and 2026. Source: Reuters Refinitiv

Against the backdrop of stubborn inflation figures, the US Federal Reserve is showing reluctance to cut interest rates. However, an economic slowdown could favor falling bond yields, reduce refinancing costs and thus support the government in its efforts to refinance outstanding US debt on favorable terms. With initiatives such as the Department of Government Efficiency (“DOGE”), the administration wants to reduce government spending and shift value creation back to the private sector. In the short term, this is likely to put a strain on the labor market, as the public sector has played a major role so far, while industry barely provided any new impetus. The USA has recently benefited from two special economic cycles: the boom in artificial intelligence and massive government spending. Both effects expire. If the reform agenda is successful, there could be new prosperity in the long term — but the path to achieve this remains characterized by volatility. The change is particularly visible in the so-called “Magnificent Seven” stocks: Massive investments in artificial intelligence are increasingly meeting uncertain earnings potential. Combined with historically high valuations, there is further downside risk — a development (Figure 2) that is already having a significant impact on the overall performance of the US stock indices.

Figure 2: Annual performance of the Mag 7 Index against the S&P 500

Figure 3: Share of new jobs created in the US labor market

Europe's departure: Between ambition and dependency

While America focuses on national strength and economic self-assertion, Europe is beginning to shape its own response to the changing world order. Europe is also looking for answers — not as a reflection of American strategy, but as an independent attempt to redefine political strength and economic independence. Driven by geopolitical tensions and repeated calls to increase defense spending, a new emancipation movement is beginning to form on the old continent. The decision of the old Bundestag at the end of February to ease the debt brake in the Basic Law marked an important step. This will give the new federal government more fiscal leeway in the future to invest in defense, infrastructure and climate protection. There are currently 500 billion euros each spent on infrastructure and defense spending. Capital markets reacted promptly: German government bond yields quickly neared 3% (Figure 4), and European equities — particularly from the defense and industrial sectors — significantly outperformed their American counterparts.

Investors are increasingly predicting that these industries could be considered the main beneficiaries of a European policy turnaround. However, the market has largely overlooked the fact that Europe's economy is still strongly export-oriented — and remains closely intertwined with the US economy. A sustained weakening of US growth is also unlikely to pass by Europe's industries without a trace. Corporate bonds, whose credit risk premiums have now fallen to historic lows, and industrial stocks whose valuations are at the upper end of the long-term range, appear particularly vulnerable in this context. While Europe is seeking its new independence, America is sending signals that have an impact far beyond its own borders.

Figure 4: Yield on 10-year federal bonds

Global challenge: The return of protectionism

Europe's reorientation is taking place in an increasingly tense global environment — not least because of protectionist signals from Washington. With the new regime of significantly increased import duties, the global economy is entering largely unknown territory. The last time comparable tariff barriers were erected was almost a century ago — a time when economies were even more regional than they are today. In an era of global interdependence, the reorganization of supply chains could have far-reaching consequences. Europe in particular is facing new challenges: As an export region, the old continent is in danger of being increasingly targeted by Chinese surplus production — with potentially serious effects on an already weakened industry. What has only been reflected in trade statistics so far could be a real test for Europe's growth model in the medium term. The world is not moving apart — it is being rearranged. And Europe must first find its place in this new order. Adaptability as the key to a new market organization These developments mark the actual beginning of a turning point in which adaptability and strategic vision are becoming indispensable for investors. Similar to Europe's search for greater independence, capital markets are also at a fundamental turning point. Both on this side of the Atlantic and on the other side of the Atlantic, there are signs of far-reaching political and economic rearrangements — with an uncertain outcome. For investors, this means that the time of simple, linear developments is over for now. In an environment characterized by geopolitical tension, fiscal paradigm shifts and structural uncertainties, broad diversification is becoming of central importance. If you distribute your investments across multiple regions, sectors and asset classes, you strengthen the resilience of your portfolio against external shocks. In doing so, we rely on a targeted selection of high-quality stocks and bonds. Alternative investments and precious metals can be useful as an addition. Diversification is the easiest way to reduce market fluctuations in challenging times and is the cornerstone of a successful long-term investment strategy. This is about more than just returns. In times of growing complexity and uncertainty, another value is also becoming increasingly important — the certainty of our investors that you can sleep well even in times of disruption because you have invested broadly in high-quality global companies. We feel committed to both aspects in our daily work for our investors.

In Hansen & Heinrich Universal Fund (current equity ratio: 90.8%), we were able to use the increased volatility to generate significant stillholder bonuses. The constant collection of breastfeeding premiums helps us to minimize fund fluctuations during these phases. We are also using current market movements to expand our positions in Booking Holdings, Palo Alto, Broadcom, Costco Wholesale and Alibaba. The largest position in the fund as of 31.03.2025 was Berkshire Heathaway, the investment conglomerate of Warren Buffet. In a market environment characterized by uncertainty, the share is once again proving its special quality. While technology giants such as Nvidia and Tesla have posted significant share price losses since the beginning of the year, Berkshire Heathaway gained around 16%. Warren Buffett's consistently countercyclical approach — most recently visible in the massive reduction of his Apple position and the creation of record cash reserves of over 330 billion USD — is having an effect. Investors appreciate the conservative capital allocation and the resilience of the broadly diversified portfolio, which focuses specifically on quality stocks and short-term US government bonds. With an increasingly fragmented global economy and volatile markets, Berkshire Hathaway remains a rock in the surf. The long-term succession by Greg Abel is prepared and strategic continuity is assured. For investors (like us) with a focus on substance, cash flow and risk management, the share remains a central component in the portfolio.

The H&H Endowment Fund (current equity ratio 34%) remains a reliable anchor in our investors' portfolios even in challenging stock market times such as these. Thanks to its broad diversification across fixed-income bonds and shares from sustainable high-quality companies, the fund delivers exactly the contribution it should make — stably, reliably and sustainably. We were able to use the market movements in March to increase our positions in proven companies with a solid and sustainable business model. For example, we've expanded our investments in Palo Alto Networks, Givaudan, Salesforce, and Intuitive Surgical. Palo Alto Networks is one of the world's leading cybersecurity companies and protects digital infrastructures of companies, government agencies and private individuals. In view of the increasing use of artificial intelligence, the need for security solutions is growing rapidly — a trend from which Palo Alto is clearly benefiting. The most recently published quarterly figures were significantly better than expected by the market. In the area of sustainability, too, the company is showing how technological excellence and social responsibility can go hand in hand. Palo Alto impresses with specific initiatives, such as the Cyber A.C.E.S. educational program, which teaches children and young people how to use the Internet responsibly. On the pension side, we were able to successfully participate in a number of new issues. Our data-driven analysis approach enables us to specifically select those issuers who not only have solid financial figures, but also a convincing sustainability profile. For example, we were able to participate in new issues from Johnson & Johnson, Sanofi and Carrefour. Johnson & Johnson is pursuing ambitious ESG goals. 87% of the company's global electricity consumption already comes from renewable energy sources — as much as 100% in Europe, the USA and Canada. By 2025, all electricity demand worldwide is to be covered green. The company also plans to reduce its greenhouse gas emissions by 44% by 2030 compared to 2021.

In WowiAssets (current equity ratio: 10%), we have significantly reduced the equity ratio by taking profits at Visa, McDonald's, Deutsche Börse, Deutsche Telekom, Allianz, MSCI and a European ETF for standard stocks. On the pension side, we reduced the share of corporate bonds through sales. The current risk premiums for European corporate bonds are at the lower end of the historical valuation and are therefore less attractive to us than, for example, European government bonds or Pfandbriefe. We were able to significantly strengthen these two segments with our latest transactions. For example, we recently bought bonds from issuers Norway, France, Poland and the European Union. Further bond purchases focused on state-related issuers such as the French company La Poste and a newly issued Pfandbrief from DZ HYP. For the current month, cash inflows, primarily in liquidity, were reserved for future transactions. The liquidity ratio as of 31.03.2025 was approximately 5.60%.